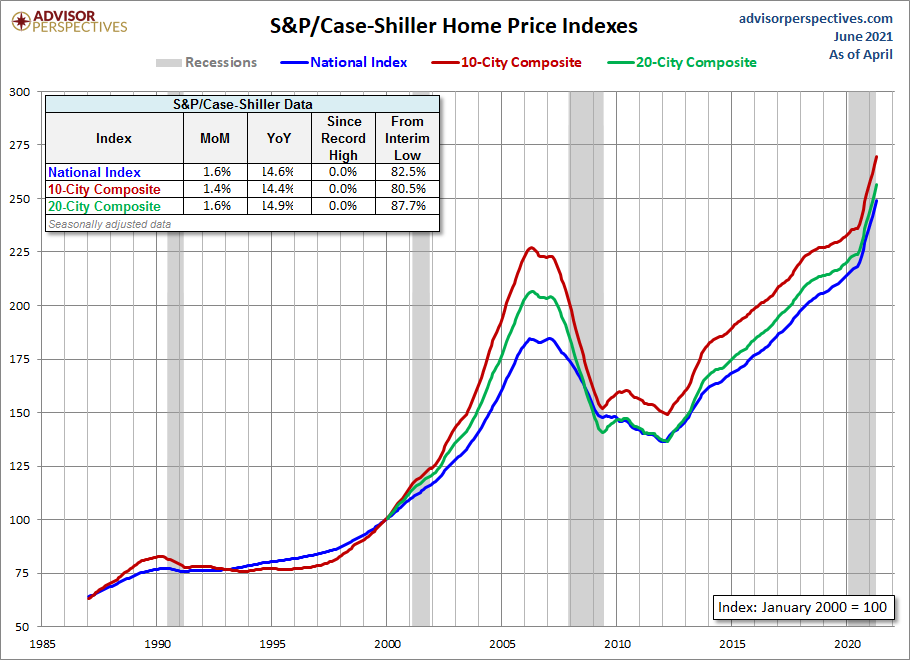

If you keep tabs on the real estate markets, you would know how crazy home prices have gotten, especially in coastal cities.

I live in Seattle and have seen home prices more than double, making it impossible for regular people to afford a decent living.

The explosive growth in the tech sector is one big factor that has fueled housing prices to reach such unprecedented levels.

Big tech companies like Amazon, Microsoft, Facebook and Google have seen their stock prices rise 5-20 fold in the matter of a decade.

The employees of these tech companies have built unsurmountable amounts of wealth through their stock grants, which were then invested into real estate.

It goes without saying that the population at large wasn’t as lucky. Overall, wages have barely risen over the past decade making housing unaffordable for most.

With that said, here are my top reasons to not buy a house in major U.S. cities right now.